I went to the 2026 Orange County Regional Economic Outlook expecting a regional macro conversation: housing, labor, AI, inflation, supply shocks, and the usual question of whether Orange County can keep growing. I left thinking about intended parents.

That may sound like a strange bridge, but it is the bridge I kept seeing in the data. Family building is deeply personal. ART is medical. Surrogacy is legal, ethical, and relational. But none of it happens outside the economy. The timing of an egg retrieval, the decision to preserve fertility, the choice to use donor eggs, the ability to keep insurance coverage, the cash reserve for a transfer cycle, the escrow plan for surrogacy, and the willingness to begin a multi-year path all sit inside the same household balance sheet.

I am a UCLA Anderson alumnus and serve as an advisory board member at the Price Center for Entrepreneurship. That is one reason I try to stay close to economic rooms, not just healthcare rooms. Fertility care is not only a clinical service. It is a planning system for families making irreversible decisions under uncertainty.

At the 2026 Orange County Regional Economic Outlook on April 29, 2026. The event materials included UCLA Anderson Forecast, UCI Paul Merage School of Business, and UCLA Ziman Center for Real Estate branding.

My Forecast

IVF will keep becoming more mainstream as a share of family formation, but access will stay uneven. Surrogacy will not become a volume story; it will become a trust, legal certainty, and planning story.

The Orange County forecast does not prove that IVF demand will rise. It does not predict surrogacy volume. It does not tell any family what to do. What it does is make the planning environment visible: high fixed costs, weak job creation, aging demographics, falling birth counts, expanding healthcare employment, and a benefits landscape that still leaves many families exposed.

1. Orange County Is Prosperous, But The Family-Formation Math Is Tight

The local Forecast materials described a county with output and income strength but very limited job creation. Orange County lost about 1,600 jobs in 2025, while healthcare added roughly 11,000 jobs and carried most of the positive job growth. The same materials pointed to a stubborn housing market: high prices, low affordability, and a regional pattern of families leaving for more affordable places.

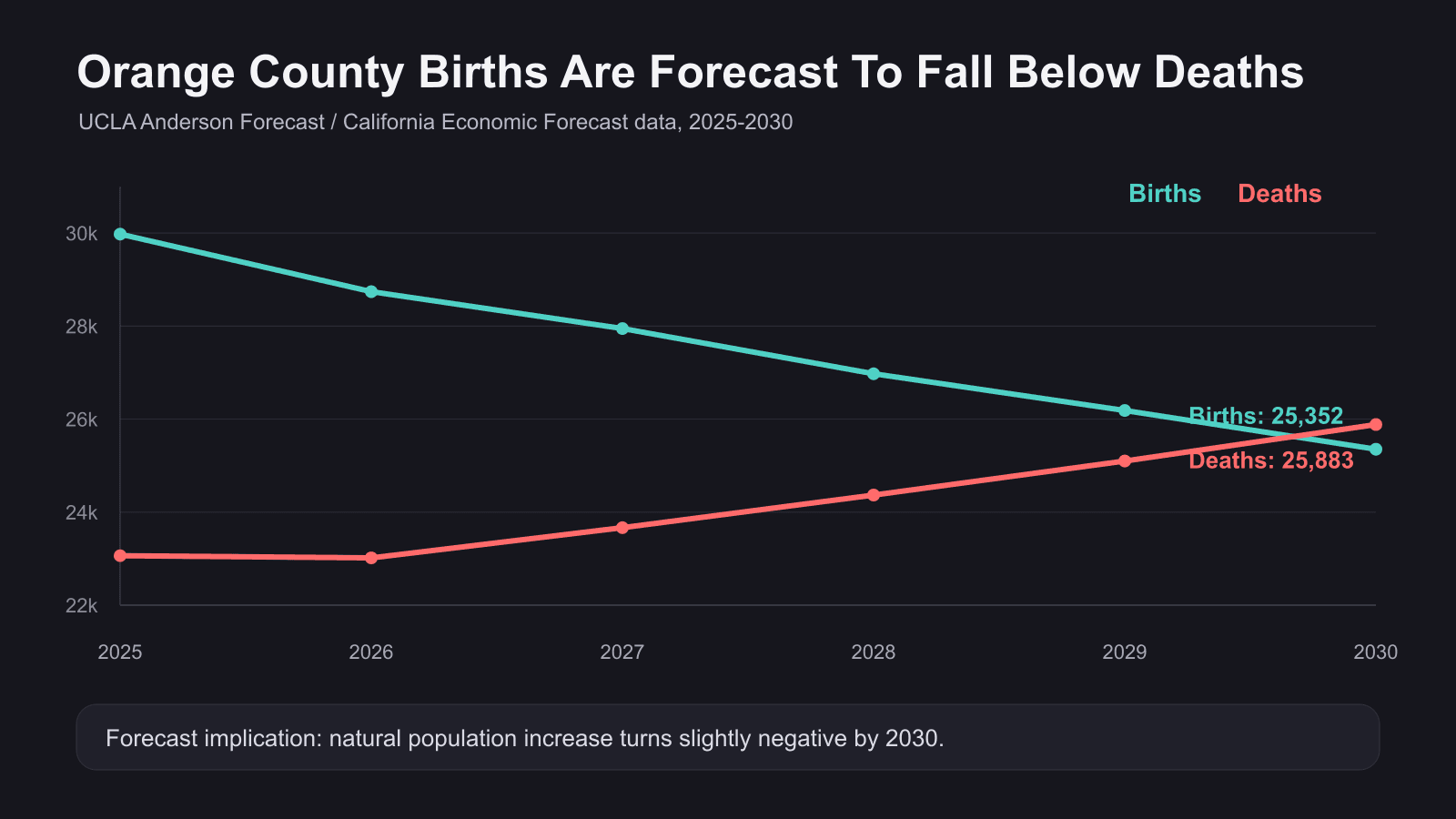

The demographic section is where the ART relevance becomes clearest. The forecast shows births falling from 29,977 in 2025 to 25,352 in 2030, while deaths rise from 23,063 to 25,883. By 2030, the natural increase turns slightly negative. K-12 enrollment is also forecast to keep falling, after a long decline tied to fewer births and family outmigration.

Original chart from the newsletter draft, using data from the UCLA Anderson Forecast / California Economic Forecast Orange County demographic table.

That is not an IVF chart. It is a family-formation chart. It says the region is struggling to keep families in place and to replace its population naturally. In a high-cost county, the decision to have a child is increasingly entangled with housing, commute patterns, job security, parental age, and liquidity.

2. IVF Has Crossed A Mainstream Threshold

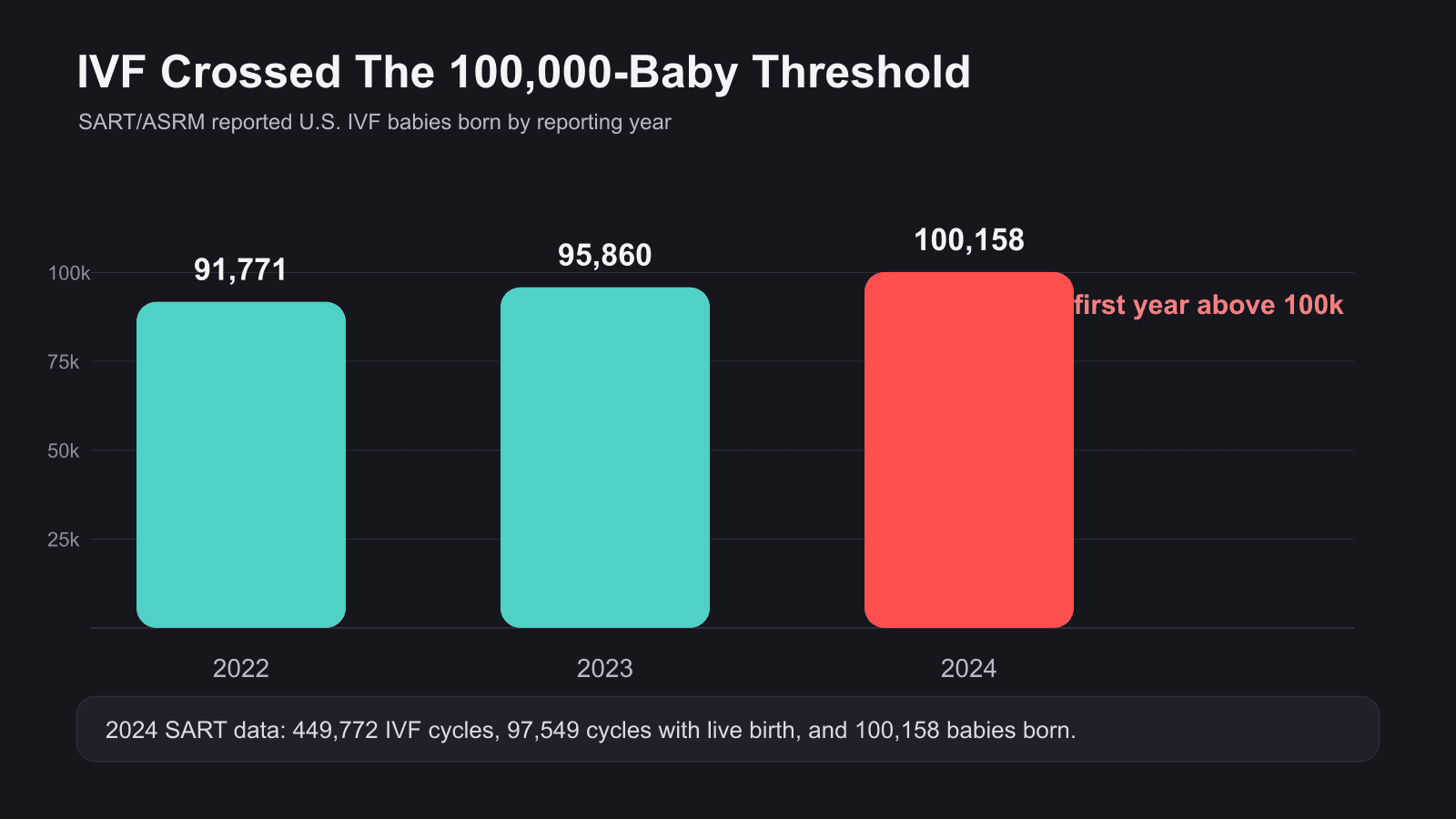

Nationally, the ART picture is moving in the opposite direction. SART and ASRM reported that 2024 data showed 449,772 IVF treatment cycles, 97,549 cycles with a live birth, and 100,158 babies born through IVF in the United States. That is the first year above 100,000 IVF babies in a single year.

Original chart from the newsletter draft, using SART/ASRM 2022-2024 IVF baby counts.

This is happening while total U.S. fertility remains weak. CDC/NCHS final 2024 data show 3,628,934 U.S. births, up 1% from 2023, but the general fertility rate declined to 53.8 births per 1,000 females ages 15-44. In plain English: more babies were born in 2024 than in 2023, but the rate at which women of reproductive age had births still fell.

That combination matters. ART can grow as a share of family formation even when the overall birth market is flat or shrinking. The market is not just people who already use IVF. It includes people delaying parenthood, people preserving fertility, LGBTQ+ families, single parents by choice, cancer survivors, people using donor eggs or donor sperm, and intended parents who need a gestational carrier.

3. The Access Problem Is Still The Business Problem

KFF found in its 2024 Women’s Health Survey that 13% of reproductive-age women said they or a partner had ever needed fertility services, 10% had received services, and 3% needed care but could not obtain it. Cost was the leading reason. KFF also reported that only about 27% of large firms offering health benefits covered IVF services in 2024.

This is why I think employer benefits will remain one of the most important channels in fertility care. Families do not only ask, “Can I medically do IVF?” They ask:

- Will my plan cover diagnostics, medications, retrieval, transfer, and storage?

- What happens if I change jobs mid-cycle?

- Does my employer renewal date matter?

- Does coverage apply to donor gametes, fertility preservation, or gestational carrier-related services?

- How much cash do we need if authorization, reimbursement, or timing breaks?

In a low-fire, low-hire labor market, these are not administrative details. They are part of the emotional risk families carry before they ever reach the clinic.

Event photo from the labor-market section. I am using it here as regional context, not as fertility-demand evidence.

4. California Is A Case Study In The Next Coverage Fight

California’s SB 729 is a major 2026 signal. The law requires large-group health care service plan contracts issued, amended, or renewed after implementation to cover infertility diagnosis and treatment, including up to three completed oocyte retrievals and unlimited embryo transfers when medically appropriate. It also prohibits denial based on participation in services involving a donor, gestational carrier, or surrogate. The California budget process later delayed implementation to January 1, 2026 for large-group coverage.

The important lesson is not just California. It is the gap between public support for IVF and paid access to IVF. State mandates help, but they do not solve every plan type, every employer structure, every service category, or every family pathway. The next coverage fight will be less about whether people say they support IVF and more about who pays, what is included, and whether third-party reproduction is treated as real family-building care.

5. Surrogacy Will Be Judged By Trust, Not Volume

ASRM’s policy framing is useful here: gestational carrier care remains a specialized modality within ART, governed by state law, FDA requirements, and clinical guidance. ASRM cites GC pregnancies as a small share of deliveries and emphasizes safeguards such as informed consent, independent legal counsel, medical decision-making authority for the carrier, and single embryo transfer when recommended. That is the right lens.

Surrogacy is not going to be evaluated like a consumer marketplace where more volume automatically means more success. It will be evaluated by whether families, carriers, agencies, clinics, lawyers, escrow providers, and courts can trust the process. Parentage clarity, funds flow, insurance continuity, clinical standards, psychological screening, and contingency planning will matter more, not less, as the public conversation around embryos and assisted reproduction becomes more politicized.

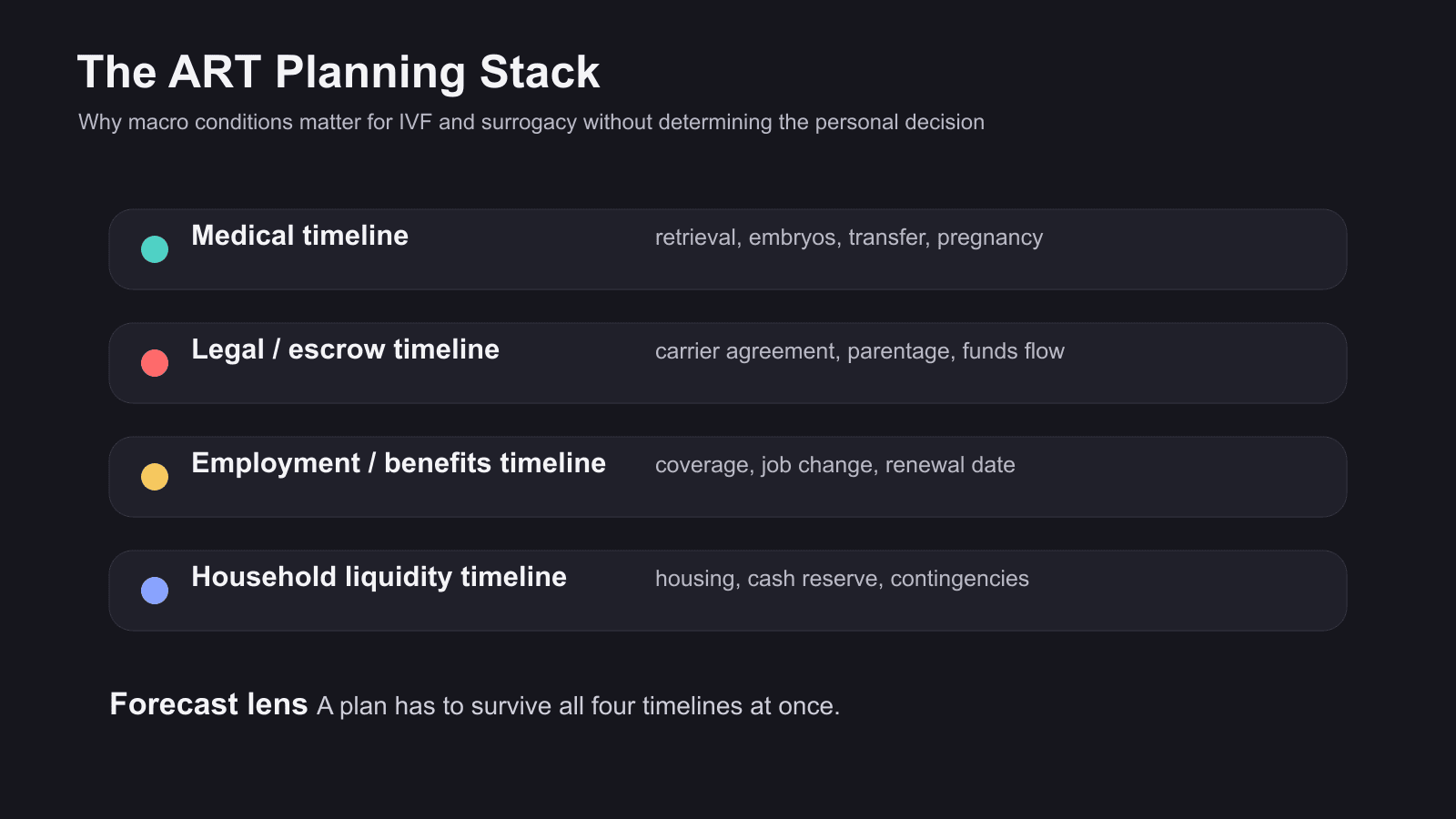

The Planning Stack

For ART, the question is not just medical eligibility. It is whether the plan can survive timing, benefits, liquidity, legal, and emotional uncertainty.

The practical planning lens I would use with intended parents: medical timeline, legal and escrow timeline, employment and benefits timeline, and household liquidity timeline.

This is where I think fertility organizations can do better. Too much of the journey is still explained in silos. Clinics explain clinical steps. Lawyers explain contracts. Agencies explain matching. Benefit managers explain coverage. Escrow providers explain payments. Families experience all of it at once.

The best operators in ART and surrogacy will not only be the ones with good individual workflows. They will be the ones that help families understand the entire plan before the expensive and emotional parts begin.

My 2026 Forecast For IVF And Surrogacy

- IVF keeps gaining share of family formation, especially as parenthood shifts later and egg freezing, donor eggs, embryo banking, and frozen transfer workflows become more normal.

- Access remains stratified. Employer benefits and state mandates expand the front door, but cash-pay families, small employers, self-funded plans, Medicaid populations, and nontraditional family pathways still face uneven coverage.

- Surrogacy grows as a trust-and-coordination category. The winning standard is not speed. It is informed consent, carrier protection, legal clarity, parentage certainty, clean escrow, and disciplined case management.

- Legal risk becomes operational risk. Embryo law, storage rules, lab liability, state parentage rules, and insurance treatment of third-party reproduction will shape family decisions in practical ways.

- The strongest fertility teams will talk about timing and money earlier. Not because families need more fear, but because late surprises are cruel.

Closing Thought

The forecast does not tell families what to do. It tells advisors what pressures families are already carrying.

In a high-cost, low-certainty environment, the most compassionate fertility guidance is not optimism. It is disciplined planning.

Source Notes For Editing

- Local event materials in Issue 2: UCLA Anderson Forecast 2026 Orange County Regional Economic Outlook book, U.S. deck, California deck, and event photos. The ART and surrogacy thesis is my interpretation of the economic context; the local event materials do not directly discuss IVF or surrogacy.

- SART/ASRM 2024 national IVF release: 100,158 babies born through IVF in the U.S.

- CDC/NCHS final 2024 birth data: 3,628,934 births and GFR of 53.8.

- KFF 2024 Women’s Health Survey on fertility-care need, access, cost barriers, and employer IVF coverage.

- California SB 729 bill text for infertility and fertility-services coverage.

- ASRM gestational carrier policy overview.

Get the next one in your inbox.

Subscribe for new issues. Unsubscribe anytime.

One email. No spam. Unsubscribe anytime.

Privacy policy